Dissecting the Innoscripta bear case

Discussing several bearish arguments, interview with the CEO and valuation

IPO = It’s probably overpriced, or at least that’s what often happens when a company comes public. Shares usually trade at high multiples, with growth rates and cash burn while insiders dump their shares. For innoscripta you could argue that it’s similar: Shares are down 40% since IPO and the founders took out over €200 million of their holdings (we’ll ignore the fact that they went public around a 22 PE for the sake of the argument). I’ve owned innoscripta for a few months now and haven’t done too well being invested. The company had some interesting updates lately, so what better time to dissect the common bear cases floating around. Check out my previous innoscripta analysis here.

I am also excited to share snippets of a conversation Burn The Index had with the CEO recently, which gave great insights. It’s important to note that innoscripta’s leadership is pretty discrete and you can’t find an image of the founder online. Another great example was that nobody from the company was present when they went public in Frankfurt. With that being said, thank you again Burn The Index (subscribe to him!) and let’s get into the weeds of innoscripta.

Very short introduction of the company

I analyzed the company in the linked post, so I’ll keep this very brief. Innoscripta is a consulting software hybrid that developed its Clusterix software platform to structure, record and submit R&D data for (so far) German customers. Like many other countries, German introduced R&D tax credits, which aims to drive innovation in Germany…but of course that comes with lots of bureaucracy. Innoscripta handles that and takes a cut of the received tax credits, making it a risk free win/win situation for the customer: if the application fails nobody gets paid. Typically innoscripta manages to find more eligible cases and optimize the tax credits companies receive. It’s a highly regulated process, so vibe coding a solution is unlikely to generate great results, while excel based solutions are only feasible for small teams <10 people (innoscripta doesn’t target those customers). Or in the words of the founder:

Burn the index: What is Innoscripta’s edge?

Mr Hohenester: I wouldn’t call us advisors because we create the documentation for the customer. We are more than an advisor by helping to structure data as a data integrator. Part of our edge is that our platform is integrated with SAP interfaces and time-tracking systems, which is very comfortable for the clients. Something a traditional advisor without software simply cannot offer. It is a bit like the competition is selling cars without wheels or engines. You buy the body from them and have to bring the rest yourself. With us, you get the whole car because we take the data and create the actual documentation. We haven’t even fully utilized our pricing yet because we offer such high added value compared to consultants who don’t have software and don’t even know how to structure the data.

The bear cases

Innoscripta got swept up in the SaaSpocalypse and shares got crushed. There are a few (more or less) good bearish arguments floating around:

Fake skin in the game

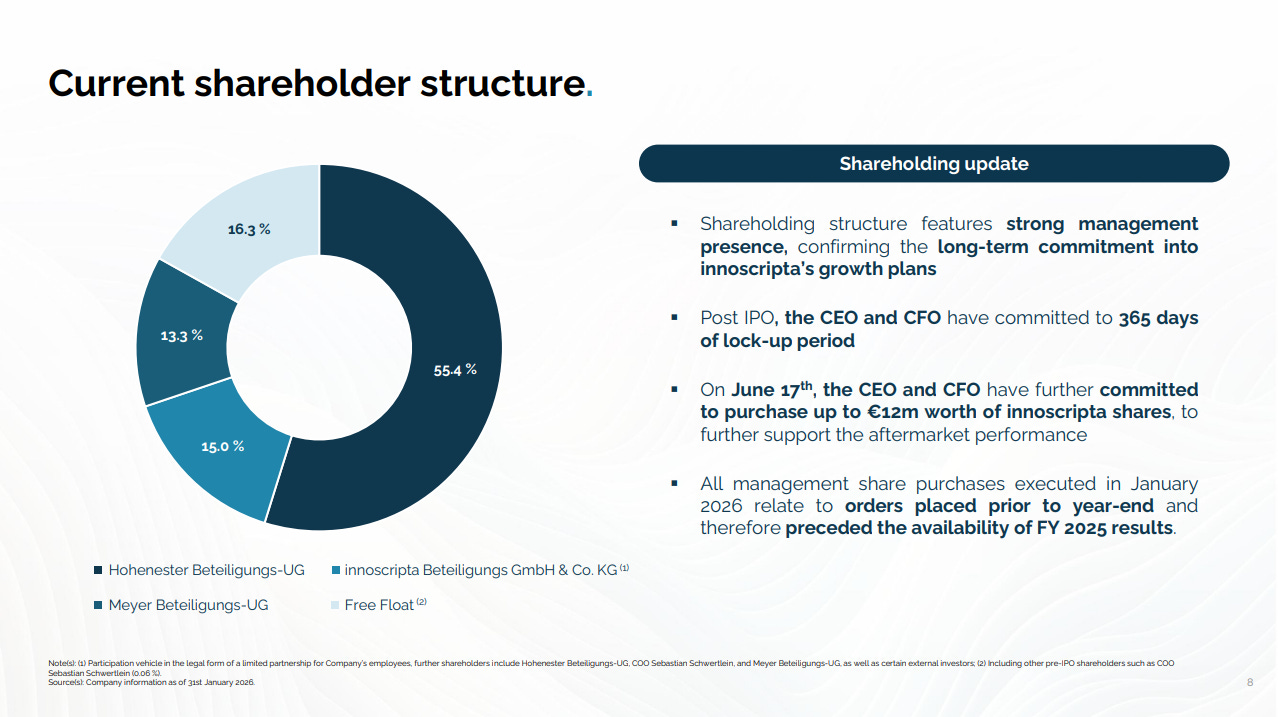

Let’s start with arguably the weakest point. Founders cashed out over €200 million euros with the IPO and paid out pre-IPO dividends over €50 million. That’s a lot of money, so the commitment to purchase around €12 million in shares on the open market following the IPO isn’t a sign of confidence. Some bears are calling it trying to prop up the share price until they can exit their position to dump on retail.

Yet we still have an incredibly high insider ownership of 84% split between management and 15% with innoscripta employees. Despite the €200 million taken off the table, Mr. Hohenester still owns over €400 million and Mr. Meyer almost €100 million in shares. They also adopted a Constellation Software-like compensation structure, where employees need to buy shares on the open market with parts of their bonus.

The lock up period is now over (24th May 2026) and we haven’t seen shares dumped from the founders. Instead we’ve seen them pay out all earnings as dividends. Some people would say that’s founders using the company as a piggy bank, but innoscripta runs a capital light structure that they really don’t need to retain cash. One negative point is that they use factoring the accelerate cash collection. Otherwise working capital would look a lot worse (success fees partially only come once the government actually pays out the cash, which can take a while). I’d say these fears aren’t justified.

One argument for this bear case could be this linkedin post, where an advisor who helped take innoscripta public mentioned that the founders were looking for an exit as early as 2020. If they eventually want to fully exit they’d probably want to do it at a higher valuation.

Regarding this question, I’ll also take the founder Michael Hohenester by its word:

Burn the index: Is there a scenario in which a take-private is on the table?

Mr Hohenester: I currently own 66% of the company directly and indirectly, and while I don’t plan to expand that share further, I’m also not selling any shares. Whether we go private again really depends on what the stock price does over a long period of time. At the moment, I believe we are too cheap. We’re currently trading at a multiple that I find far too low, but I expect the market will eventually honour our results with a double-digit price-earnings ratio.

[…]

We find the IPO was very meaningful for our reputation and transparency, which helps us displace competitors, and we want to maintain the listing to provide liquidity for our employees as part of our ownership culture.

We can see that he acknowledges the cheap shares and eventually expects the market to recognize this. The fact that he acknowledges a possible take private in the future could actually be the bear case rather than insiders dumping in my opinion: A cheap take private is much more painful than insiders dumping expensive shares on you (from the point of view of an investor at the current price as entry).

German regulations will destroy them

This is probably the most important bear case, because (right now) it could absolutely cripple the company. I see innoscripta as a binary bet actually: If Germany decides to discontinue the Forschungszulage (R&D tax credits), then innoscripta would see revenues fall close to zero. But what’s the probabliliy of that?

The political support for the scheme is unusually strong for German standards. There are some differences in emphasis between the parties:

CDU/CSU generally favor a more generous and business-friendly tax credit regime to improve Germany’s competitiveness.

SPD supports the instrument as part of industrial policy and innovation promotion, while often emphasizing support for SMEs and domestic employment.

Greens support innovation incentives, particularly for climate and digital technologies, although they tend to prefer combining tax incentives with targeted subsidies.

Parties on both the left and right occasionally criticize the administrative burden or distributional effects, but abolition is not a mainstream position.

The last point is a threat: If they’d actually make the buerocracy behind the process a lot easier, then innoscripta would probably lose business. “Fortunately” (for innoscripta) developments in other countries like the UK show that too lean rules lead to abuse. The UK has strengthened the administrative burden after companies abused it. Germany likely will have taken notice from that and will keep its position as the world leader in administrative burdens (not a great leadership to hold).

HMRC’s latest error and fraud estimates, published in its 2023 to 2024 ARA, show that in 2021 to 2022, of £7.6 billion claimed, the overall level of error and fraud was £1.3 billion (17.6%). Of this, £1.2 billion was in the SME scheme (25.8% of the expenditure in that scheme) and £134 million in the R&D expenditure credit (RDEC) scheme (4.6% of expenditure in that scheme).

Since its introduction in 2020, Germany's Forschungszulage has enjoyed broad cross-party support and has been repeatedly expanded. The trajectory suggests that the program is evolving from a modest tax incentive into a cornerstone of Germany's industrial and innovation policy. Maximum caps increased from €500k in 2020 to €2.5m for large companies and €3.5m for SMEs in 2024 and further expanded to €3/€4.2m in 2026. Alongside the cap increases there have also been expansions of what’s eligible (i.e. some depreciation expenses have recently become eligible). Overall, we’ll likely see increasing caps. Especially for large enterprisees, the cap is pretty low. Volkswagen for example spends many billions annually on R&D, yet can’t regain more than €3 million right now.

Innoscripta is looking to mitigate the risk of regulation destroying the business by going international. A few days ago they announced their first customers wins (very certainly >€1 million in revenue for them to make this press release) in France, just a few months after setting up shop there. Their easily modifyable software makes entries into new geographies easy, giving them an advantage.

Lastly, I’ll refer to the interview below, where it’s clear that the international runway to grow within existing multinational customers is huge. A single customer with 20-30 million in revenue would make up around 15-20% of revenue today. Expansion into other highly regulated workflows, where a papertrail is required also is in development. So over time innoscripta should become a much less risky business, but today we are not there yet.

Mr Hohenester: The German market will continue to grow for a very long time, but we do not want to rely solely on this market due to the risk of legislative changes that could make the market less attractive. We’re not expecting any changes, but we want to be ahead of the curve. I think that international expansion is a necessity to maintain Innoscripta’s growth trajectory over a long term period. Countries like the US, Canada, Japan, Singapore but also Japan offer great opportunities. We also see an opportunity in selected European countries. Some of these markets are significantly larger than Germany. We do not blindly walk into these countries. We assess them in advance based on a set of demand and legislative criteria.

Burn the index: How do you see the sales organisation scaling?

Mr Hohenester: I see several possibilities for scaling. One major path is growing internationally with our large existing customers. Take [REDACTED] as an example: they started with us in Germany as a trusted partner, and now we can go to the USA and handle their research allowance there. If we were to truly and fully roll out that model worldwide with a single customer like [REDACTED], it could yield €20 to €30 million in turnover. To support this, we need different sales and expert teams so we can eventually cover the whole world and serve these multinational corporations. At the same time, we are building specialized teams around the Office of the CFO. We are currently testing a software solution for transfer pricing (Verrechnungspreise), which has incredibly high synergies with our current work. Transfer pricing is a complex theme. Companies like e.g., [REDACTED] must justify the prices of goods, like diesel engines, sent between international branches to various tax authorities. This requires endless documentation, and if it doesn’t fit, companies face significant back payments. We have several such ‘irons in the fire’ where we want to grow on the product side. By increasing the breadth of our offering, we create a much larger value proposition.

innoscripta has no moat

Many people question innoscripta’s moat in times of AI, where a workflow like their could be vibe coded (in theory). In reality innoscripta might not have the biggest moat, but they have a first movers advantage and seems to be an innovation first company with new tech stack. Their workflows are harder to automate, because it isn’t pure software but needs consulting on top to set up the workflows. They basically sell the trust in having a good process to get the credits, versus vibe coded solution that likely won’t get approved by the strict government regulations.

Burn the index: AI will apparently take over the world, but also Innoscripta?

Mr Hohenester: We offer a solution to a complex problem which also involves large sums of money which are critical to our customers’ ability to operate. This complexity is also the number one killer for AI incumbents. Because we deal with taxes, it is a matter of trust and complex technical work, which keeps others from easily jumping over that hurdle and rebuilding what we have.

The Big 4 accounting firms on the big accounts and tax consultants on the small accounts are competition, but Clusterix has good demand and increasingly so just to understand the own business of customers better (customers that buy the software without intention to reclaim R&D tax). Innoscripta is a show me story, we need them to continue executing to understand if it’s just first movers advantage or if there’s a durable competitive advantage. So far it’s looking good however.

Burn the index: What is the biggest challenge?

Mr Hohenester: Getting admitted to the Office of the CFO is a high hurdle because the Big 4 tend to have a foot in the door. We have been increasingly successful in Germany by outplaying them. It’s also interesting to see that we our handed over projects where competitors failed.

Are margins sustainable?

Another bear case is that they are overearning right now and that margins will come down. Through a sharp focus on its cost structure and profitable growth, innoscripta has built a very capital light, scalable and profitable company. Right now EBIT margins are above 63% and the question of course is if they can remain this high.

The best argument for declining margins are that they are opening offices in other countries, which will need time to contribute to revenues. Sacrificing margin for growth is a great trade off though looking at the opportunity ahead. The fact that they are against M&A for the sake of it (they looked but didn’t find suitable targets) and instead are growing organically shows their discipline as well. I’m confident that we’ll have (if not these peak margins) a highly profitable business at a much higher revenue base in a few years.

After we addressed the common bear case for innoscripta, I now want to shift gears towards the valuation of the business. I own shares and bought more after the news of confirmed French clients, so obviously I find it cheap enough to own. I’ll also provide the transcript for the full interview below. Once again, thanks to Burn The Index for the great conversation and collaborating on this article.

Now let’s get straight to the numbers:

Valuation

| A guest post by

|