Eurofins Scientific: Can this Elite compounder get back to outperforming?

Despite its three year bear market the company delivered a 28% CAGR over the last 25 years.

Over the last 25 years, there have been few companies that have delighted investors more than Eurofins. The company returned a 28% total return CAGR, only beaten by Amazon, Apple and Monster Beverage. Over the last five years however, the company returned just 8% and has crashed over 50% from its bubble peak in 2021. Let’s find out what’s the reason for this underperformance and if fundamentals indicate a bright future again.

You can read the first part of the analysis here.

What has Covid done to the business?

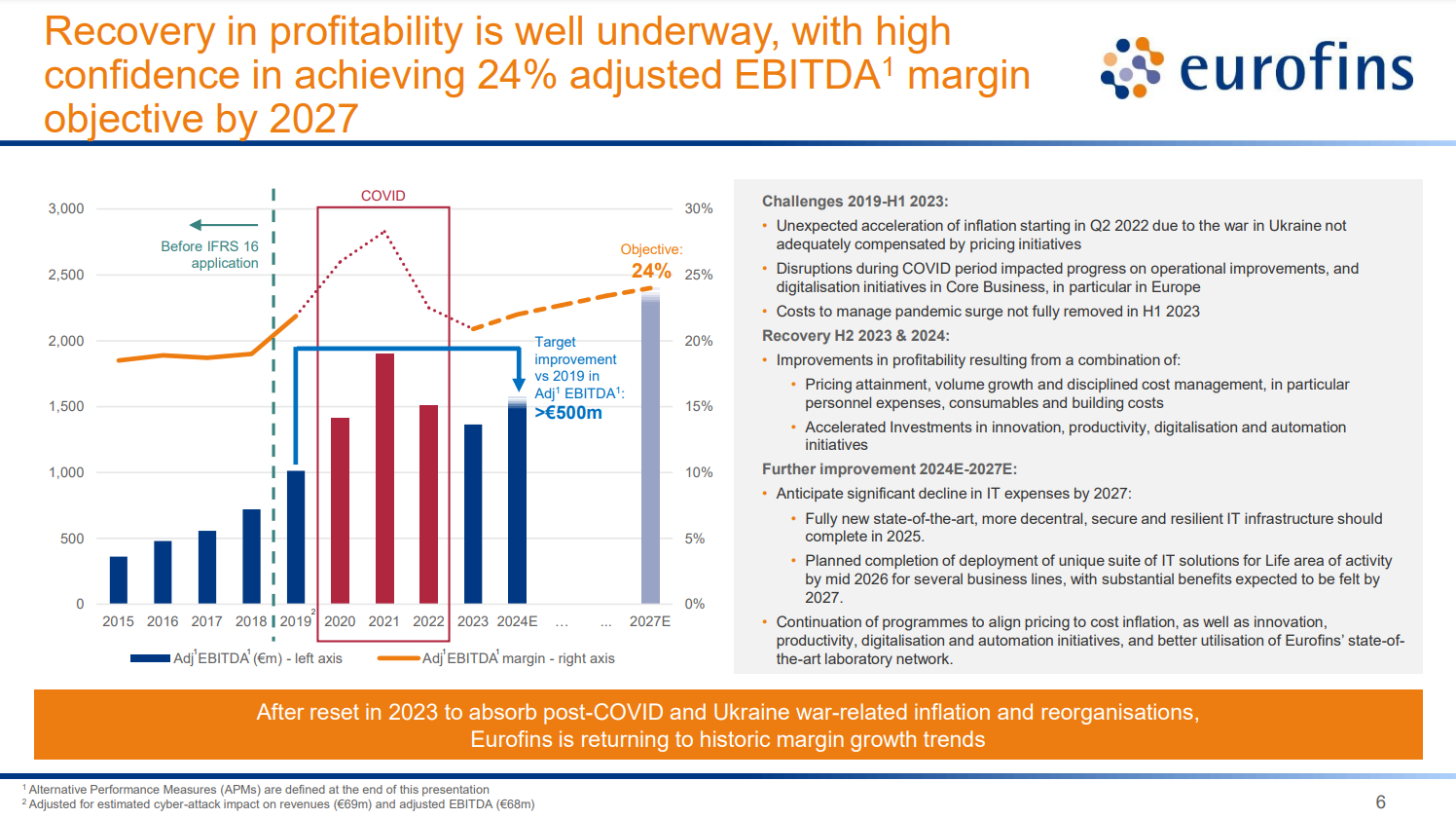

The COVID-19 pandemic was a once in a century situation that disrupted many industries, especially the critical life sciences industry. As a provider of various laboratory testing services, Eurofins naturally was a strong beneficiary of this situation. The company made sure to bring a lot of capacity online as fast as possible to service this large demand. 2021, when COVID testing became readily available, was a record year, seeing revenues and margins skyrocket. The company had no problem filling its labs with orders and could utilize its capacity at maximum, generating high growth and Returns on Capital Employed (ROCE).

As the pandemic became endemic and not the primary focus of public safety, orders regressed and the windfall profits subsided. Eurofins now was left with rushed capacity, but lower orders. This naturally resulted in a compression of revenues and margins. Everybody that analyses Eurofins should be aware of this situation and not take the 2020–2022 results at face value. We need to look at long term trends instead.

What’s next?

How efficiently does Eurofins use its capital to generate returns?

What’s Eurofins quality score? Where does the company excel and where does it struggle?

Can the blog buster performance of the last decades be remotely repeated?

Would I buy Eurofins at these prices?

We’ll discuss this and more in the premium section of this analysis.