Pluxee with stellar H1 results

First earnings report as a public company

Pluxee reported its first quarterly results as a public company this Friday, beating expectations and raising guidance. After an initial 10% pop, shares slid down to a 5% gain as the overall market slumped throughout the day. Here are my previous analysis on the Business model and the fundamentals & valuation.

For H1 24, revenue came in at a strong 24% organic growth, with EBITDA increasing to 201 million euros (up 23%). Recurring FCF came in strong at 228 million for the quarter, 113% of EBITDA. However, FCF is distorted, and I’ll discuss profitability and cash flows in the valuation section of this article.

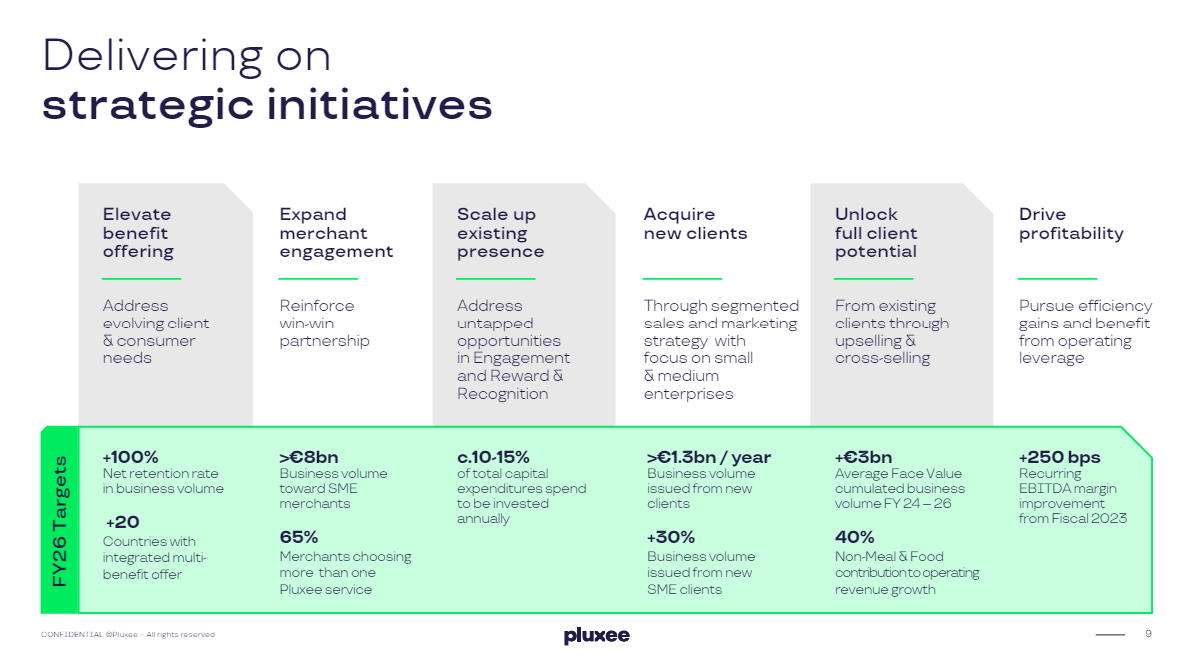

Pluxee set up a roadmap with targets for its business through FY 26. The roadmap can be summed up into:

Expand offering and merchant network (I’ll focus on the other ones today)

Grow new and existing clients

Operating leverage through investments

Grow new and existing clients

In H1, Pluxee managed to grow Business Volume Issued (BVI) by 0.85 billion euros to 12.4 billion euros, compared to the target of 1.3 billion for the full year, well-exceeding expectations. The growth came especially from Continental Europe (Belgium, Romania and France in particular) and Brazil. SME clients contributed around 25% of the gained volume and are on track to reach the 30% target for FY 26. Remember that SME clients represent a huge opportunity due to the presently low penetration: In the past, it was hard for small businesses to offer good employee benefits, but with solutions like Pluxee, this becomes easier and vital in the war on talent where employees seek meaning in their work and a good employer. Presently, Employee benefits account for all of the growth (8.3 billion to 9.2 billion, growing 12%), while other products and services are lapping tough comps from public benefits programs issued over Q1 23 and saw BVI in the segment decline from 3.5 billion to 3.1 billion.