Stemmer Imaging Valuation and Fundamentals

Since Stemmer Imaging is getting acquired, I decided to drop the Paywall from all Stemmer Imaging articles. While the company won’t be tradable anymore, it still gives you an idea of the type of work I do for paid subscribers.

This is the second part of my piece on German machine vision microcap Stemmer Imaging. This article will look at the fundamentals and valuation of the business. If you missed the first part, here is the link.

Since its IPO in 2018, Stemmer hasn’t been a great performer. People often joke about the true meaning of IPO being “it’s probably overpriced.” This was the case with Stemmer. At the IPO, the company traded at 20 times forward EV/EBITDA, its highest valuation to date. I see, however, a great opportunity in the shares at these levels. Google shows the dividend yield at 9.12%, this is incorrect going forward and the result of the special dividend they paid out last year.

While the shares have gone sideways, the fundamentals improved significantly. Below is a 10-year historic P&L, which the company shares in its presentations. The green dotted line indicates the IPO. We can see that revenues have increased by 50% since the IPO, but more importantly, earnings have increased significantly through scale and improved efficiencies, as mentioned in the first post. Management believes there is more room for improvement and that EBITDA margins (this is real EBITDA, by the way; management doesn’t like to adjust) can improve to 21% at the high point. Historically, they have lowballed expectations regarding profitability, so I wouldn’t be shocked if they raised the long-term outlook over the years.

The industry is currently in a tough spot, but these headwinds are temporary. Q4 will be weak as machine vision overstocking is still in place. Current contracts are going to ramp up in H2 2024. For FY 2023, the company guides revenue declining 3-7% with EBITDA at 26-32 million Euro. In 2024, Stemmer expects a strong catch-up effect with upper single-digit revenue growth with a similar EBITDA margin in the second half.

Over the mid-term, they share the consensus of a ~7% CAGR for their overall market. Stemmer wants to continue diversifying its business to non-industrials (with higher margins), drive efficiencies and customer satisfaction and expand its network. For 2026, the company targets 240 million sales with 17-21% EBITDA (40.8-50.4 million Euro EBITDA) and a strong focus on cash flow generation. Historically, Stemmer had a good conversion from EBITDA to cash flow. Stemmer added that they had assumed 30 million of M&A within the 240 million sales target. They are currently in talks with several potential acquisition targets within regional and technological expansion targets and could already see a deal close in H1 2024. The last M&A deal was Infaimon in 2019 to scale the expansion into Spain and LATAM. Hopefully, we can see a deal sooner rather than later, but I also appreciate that management is diligent and is waiting for the right pitch. Stemmer has 33 million in Cash and short-term investments versus 8 million in debt (primarily leases), so a large deal would be possible. If the opportunity is right, they could also see a deal done with a share component.

Let’s talk about capital allocation a bit more. Stemmer has a pretty easy framework:

Focus on organic growth

Enhance it with selective M&A if it makes sense

Pay out dividends (70% payout ratio)

Manage debt

The big pain point I have is the 70% dividend payout ratio and that management is categorically against share buybacks like many German companies are. I prefer it if money is reinvested in the business, and a 70% payout ratio could hinder this. On the bright side, Stemmer is very profitable and has a capital-light business model. CapEx is pretty low, between 0.5 and 2 million a year. The biggest capital need is within working capital, and 15/20 million of net working capital is inventories (makes sense for a distributor). Historically, NWC/Revenue stands around 15%, and the company is focused on managing this ratio to increase cash flows. Stemmer has a fast cash conversion cycle of about 70 days compared to other distributors I follow, like Watsco, Ferguson, or AO Johansen (I’ll write about them next). While the comparison isn’t apples to apples, it is a rough guide. The business can afford to pay out large dividends without penalizing growth. With Primepulse owning 69% of shares, some claim they use Stemmer as a cash cow with large dividends. This could be the case, but I am okay with it as long as it does not hinder the business from executing. This is probably why they aren’t looking to do share buybacks. It is a pity that the company could retire around 10% of shares outstanding yearly at these low valuations.

Stemmer has had rising Returns on Capital due to its increased profitability while keeping invested capital low by paying large dividends (reducing equity). Since IPO, EBIT ROIC rose from 12% to 31%, and Owner Earnings (OE) ROIC rose from 6% to 17%.

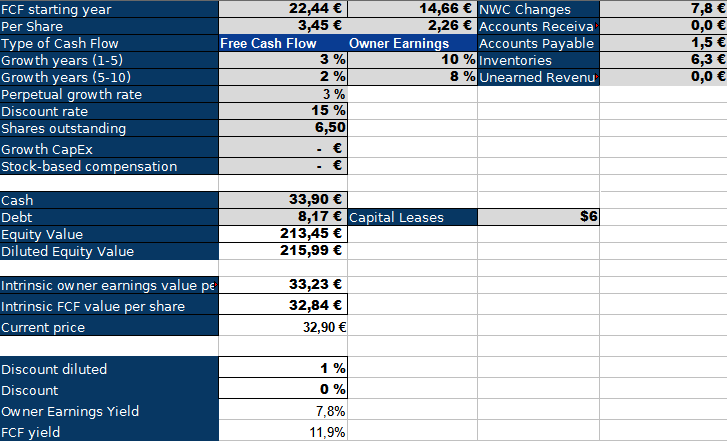

Let’s look at Owner Earnings. I define it as FCF + Growth CapEx - SBC +/- NWC changes. I did not assume any growth CapEx because they hardly have capex anyway. This is just simplifying it. The company doesn’t pay out stock-based compensation; shares are stagnant at 6.5 million (unless they use shares for a deal if needed). The large difference between FCF and Owner Earnings is from changes in inventories. As mentioned above, the industry is currently destocking, so Stemmer is also drawing down its inventories. While this temporarily lifts FCF, it is not a recurring, durable cash flow generation. Once we adjust, we go from an enterprise value yield of 11.9% to 7.8%. This is still a good yield for a company expected to grow double digits over the cycle. I used a 15% discount rate in my model and got to a 10% required growth for the next five years, followed by 8% for five years with a 3% perpetual growth rate. Is this a realistic growth rate? The industry is expected to grow by 7%, and Stemmer expects double-digit revenue growth, let’s say 10-13%.

Additionally, we have around a 10-20% incremental margin improvement opportunity. Buybacks won’t boost cash flow per share, but considering this outlook, we should get a 10-15% growth rate over the medium term. This looks quite compelling considering the compelling end market with secular trends discussed in the first article and a conservative management team with skin in the game as well as a long-term time horizon.

Valuation multiples share a very similar picture. Stemmer trades significantly below its historic valuations at 7 times forward EBITDA and 14 PE. As the business reaccelerates we could see a normalization of the valuation multiple. While I don’t like to bet on multiple expansion but rather on fundamental development, it makes for an interesting setup.

Risks

Stemmer has several risks as a micro-cap. Usually, small businesses have a hard time getting access to capital; I don’t think this is an issue for Stemmer due to its cash generation and balance sheet and access to cheap loans from PrimePulse as a majority owner.

The current downturn perfectly shows the dangers of a cyclical industry as MV/AV depends on the economy for a large part of sales, even though they are looking to diversify outside of industrials.

Additionally, the risk of new entrants into the market as its growth persists and could eventually lead to margin pressures. It helps them offer value-added services, differentiate their offering, and keep and raise margins.

Conclusion

Stemmer Imaging is a compelling investment opportunity in a well-run, stable business in a cyclical growth market with a large majority owner and a great balance sheet. The chances outweigh the risks, in my opinion, and I hold a position of ~3% of my portfolio.