February 2024 Portfolio Update

This was the first month dedicated to Substack to migrate most of my Seeking Alpha coverage and additional (European) small-cap coverage to the paid tier. This will be exclusive content to this Substack. I published a lot of content including my investment cases for ASML, Copart and AOJ. I also covered the earnings releases of Adyen, RCI Hospitality and UFP Industries. You can find more details on it here.

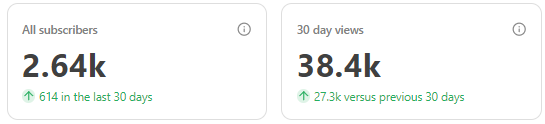

The substack saw over 600 new subscribers and almost 40k views. These results are encouraging, and I’m looking forward to continue producing great content and growing this channel. With the button below, you can get a 7-day free trial. Thank you for reading.

Portfolio Update

February saw some changes in my portfolio: I exited Ulta Beauty at a 26% gain and I started a new position in Pluxee. I explained both decisions to my paid subscribers on the same day in the linked posts with a brief investment case and valuation. I intend to continue doing this going forward. In the following days, I’ll publish my investment case and fundamental analysis of Pluxee, a leader in employee benefits and engagement.

Furthermore, I added to four existing positions in the month:

Stemmer Imaging continues to trade at attractive valuations, so I added to the position.

UFP Industries saw shares trade ~10% lower after earnings and presented a nice entry to add to this quality business.

AOJ fell 10% after earnings and has since then recovered more than those losses.

Mercado Libre has fantastic earnings but got punished for a one-time expense. Small add to the position.

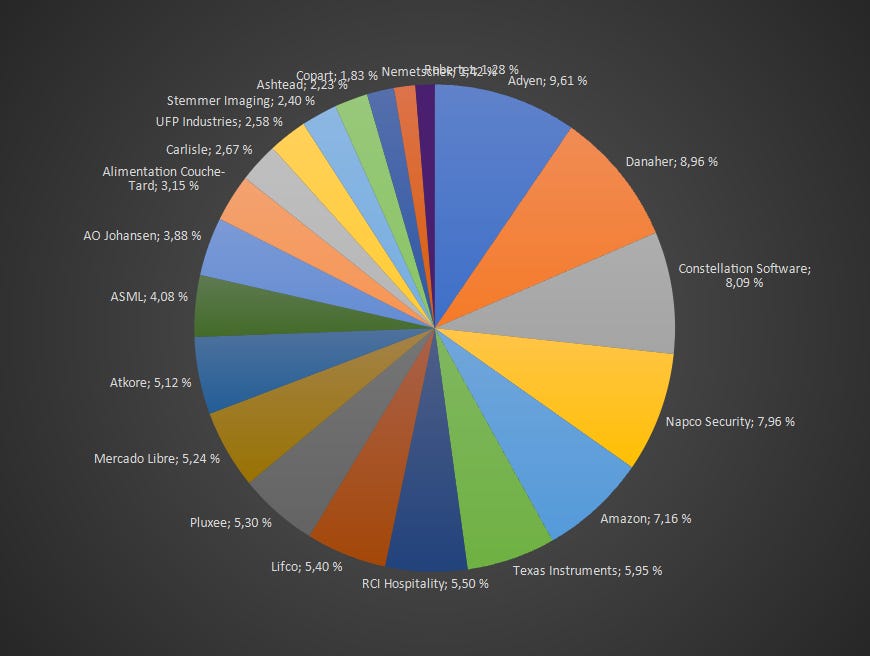

February was a good month again, with a 6.3% gain in the portfolio compared to 4.2% for the S&P 500. Year to Date the portfolio is up 10% versus 9% for the S&P. The market continues to catch steam, and I’m getting more worried about valuations; many good deals are becoming expensive again. The top contributors were Napco (27%), Adyen (24%), Amazon (13%) and Ashtead (12%). The top detractors were RCI Hospitality (10%), Stemmer Imaging (6%) and Mercado Libre (6%). A few of my holdings saw decent volatility during the month due to earnings, which I took advantage of.

I still have my eye on Texas Instruments. I’ve owned the business for 3.5 years, and the fundamental development hasn’t been great. I applaud the heavy reinvestment into fab capacity, but I am not a fan of their continued dividend payments, now almost all of the operating cash flow. TXN is looking really ugly right now, but that’s how it often goes for cyclicals: Buy when they look ugly. I haven’t done a good job of that in the past. I started my position when they were at peak margins and announced the heavy capex ramp. The recent capital management day didn’t really give any new insights. Really, management continues to just follow its plan. Probably a good sign. While I don’t think about selling the business, I wouldn’t mind having a smaller position. I hadn’t thought about this too much in February because I was occupied with other things, but it is still on my mind.

As always I’ll share the article I published on Seeking Alpha last month:

MELI 0.00%↑: Mercado Libre is accelerating its cash generation

Extremely exciting growth from you. Impressive numbers. I'll be following this growth story!