IDEXX Laboratories: The Hidden Giant Powering Pet Healthcare

The business behind your vet bill: Why IDEXX is a global leader in pet diagnostics

Ever wondered who’s making money when you take your pet to the vet? I recently found out firsthand! Last year, my girlfriend got a rescue dog, which was just a few months old. It’s been the first time I developed a real bond to an animal and I can tell that it’s a beautiful thing, but also challenging and coupled with a lot of expenses.

Naturally, as an investor, that sparked my curiosity about the value chain in the companion animal sector…. and who’s behind that $250 vet bill we just got!

There are a lot of food and toy companies, but those are largely uninteresting, without barriers to entry, and often inside large conglomerates. Two companies stand out in the animal healthcare space, both of which I’ve known but have not researched thoroughly.

Zoetis is an animal pharma company that was spun out of Pfizer and is considered a high-quality company. Unfortunately, pharma is outside of my circle of competence. Luckily, there is also IDEXX Laboratories, a highly praised global juggernaut in the Companion Animal Diagnostic market and the company responsible for the $250 bill from our blood test. The company has been on a tremendous run since it was founded in 1983 and has quietly built an incredible moat in a booming industry.

Improving animal lives

IDEXX has a wide portfolio of products and services with three focus areas to take up as much of the practice workflow as possible. IDEXX is to pet diagnostics what Visa is to payments—an entrenched leader with a massive network effect:

Point-of-care diagnostics are the devices for the actual diagnostic patient visits.

Diagnostics and Clinical Workflow data management systems to efficiently run the practice.

Reference Lab aids in test evaluation, consulting and virtual visits.

By entrenching themselves in the practice workflow, they effectively partner with the practices to foster mutual growth and high switching costs. According to a >1000 practice survey from IDEXX, practices that are engaged with IDEXX showed faster growth in average clinical visits per practice (90 bps outperformance), average clinical revenue per practice (210 bps outperformance) and average diagnostic revenue per practice (210 bps outperformance). There is a shortage of trained professionals and the average number of clinical visits per practice is increasing. Clinics NEED to use IDEXX to stay competitive.

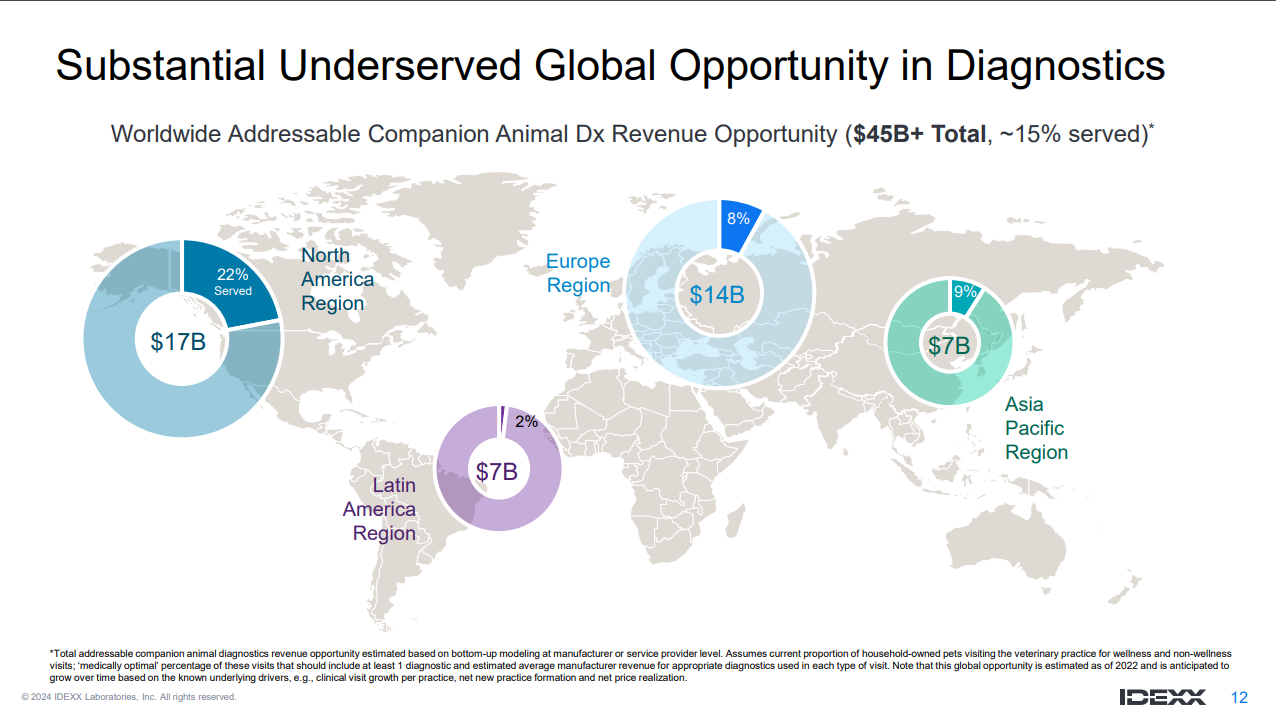

The global Companion Animal diagnostic market is estimated at $45 billion, with a very large white space. IDEXX estimates that only 15% of it is served currently ($6.75 billion in sales), with the US spearheading at 22% served, compared to single digits for Europe, APAC and LATAM. As awareness and willingness to spend for pets continue to grow, more of the market should be served over time.

IDEXX also has business in microbiology tests for drinking water safety and diagnostic tests and services to monitor the health of lifestock animals, but those are smaller segments and not material to the investment case in my opinion.

The market has several secular tailwinds:

📈The pet population is growing, expanding and aging.

🐕Pets live longer, leading to longer care periods and higher care intensity and frequency with older age.

🔬Increasing pace and impact of innovation leading to increasing standards of care.

Besides the secular tailwinds, we also saw a pandemic-induced explosion in growth in 2020: As the world locked down people became lonely and the US pet population grew at 6% in 2020 and 4% in 2021, compared to its historical 1% trend.

From an ethical POV, it’s certainly critical if we should adopt pets when we feel lonely, and we could certainly question if all those COVID pets are taken good care of, compared to the normal, more rational (in theory) process of getting a pet. However, for the industry, it’s certainly a positive.

IDEXX uses one of the most outrageous long-term projections I’ve ever seen a management team cite: a 25-year(!) sector growth CAGR of 9%, driven by 10%+ international and ~8% growth in the US. Let’s see if these projections sound realistic and if IDEXX is such a special company after all.

What’s next?

IDEXX is a highly advantaged company. In the full deep dive, I cover:

✅ Details about the large moat of IDEXX and its competition.

✅ The secular tailwinds driving the industry forward.

✅ Discussing the management team and incentives.

✅ Risks and conclusion.

If you want high-quality investment research on world-class businesses, subscribe to Heavy Moat Investments.

🔥 New to my research? Check out my free deep dive on Ashtead Group to see the level of insight you’ll get as a premium subscriber. Business model deep dive - Fundamentals and Valuation deep dive

As a premium subscriber, you’ll get:

✔ Detailed Research on high-quality global compounders and European champions, with deep fundamental & valuation analysis.

✔ Actionable Investment Pitches – Ideas with high upside potential and limited downside.

✔ Earnings Breakdowns on key reports and market reactions.

✔ Real-Time Trade Alerts on all my portfolio moves, plus access to the premium chat.

✔ Exclusive Investing Tools, including my Inverse DCF template and more.