Texas Instruments Quality Score – A Wide Moat or an Aging Giant?

Assessing TXN’s durability, capital allocation, and future growth potential.

Hey everyone,

Welcome to the third edition of my quality score format, where I break down all 13 points of my quality score framework for a high-quality business. This way we can quickly assess key qualitative and quantitative characteristics of a business.

Today we'll assess my longest holding, Texas Instruments. The company has gone sideways for the last four years and hasn't been a spectacular investment, but how might the future look like?

My Mercado Libre Quality Score post showcases how a full breakdown looks like.

Check out this post if you want more details about the quality score.

Let’s dive in!

A short introduction to the company

TI develops, manufactures and markets analog and embedded semiconductors. Analog semiconductors are very different from digital chips like GPUs. Products include power change, signal change chips, sensors or anything converting real-life signals to digital signals; every time a button is pushed, we need an analog chip. According to electronics sourcing, an average analog chip costs around 35 cents. Let's compare that to the average of $40 it takes to produce digital chips, for example, from Intel. This means that companies would hardly consider switching out a $0.35 chip for a $0.33 chip from a competitor. Analog chips have high switching costs.

The strategy is simple, in the words of previous CEO Rich Templeton:

The best measure to judge a company's performance over time is the growth of free cash flow per share, and we believe that's what drives long-term value for our owners.

If you've ever heard Rich Templeton speak, you'll know that he loves to talk about free cash flow per share but, most importantly, the long-term growth of this metric. I believe that TI has several durable and widening competitive advantages:

Large product portfolio in attractive end markets

Cost advantage through vertical integration

Geopolitically dependable manufacturing

Management Alignment (2/5)

Texas Instruments has a good track record of excellent management, but it’s tough to give its alignment a good score. Insiders own less than 1% of shares and they recently got a new CEO (he has a 20 year tenure within the company however).

The short-term incentive is a mix of revenue growth, operating profit margin and total shareholder return and there is a company-wide profit sharing program at 20% of salary for employees. The long-term incentive is time vested shares to management. Overall nothing exceptional, especially the lack of long-term targets. Management has prioritized long-term investments despite these shortfalls however.

Secular Trends (3/3)

TI benefits from several secular trends:

increasing semiconductor content—everything is becoming smart and requires more chips

reshoring—The Biden administration and now the Trump administration are want to bring manufacturing back to the USA, increasing demand for US made chips.

geodependable capacity—Similarly to reshoring, governments globally try to incentivize localized supply chains and especially chip supply outside of Taiwan due to the geopolitical situation.

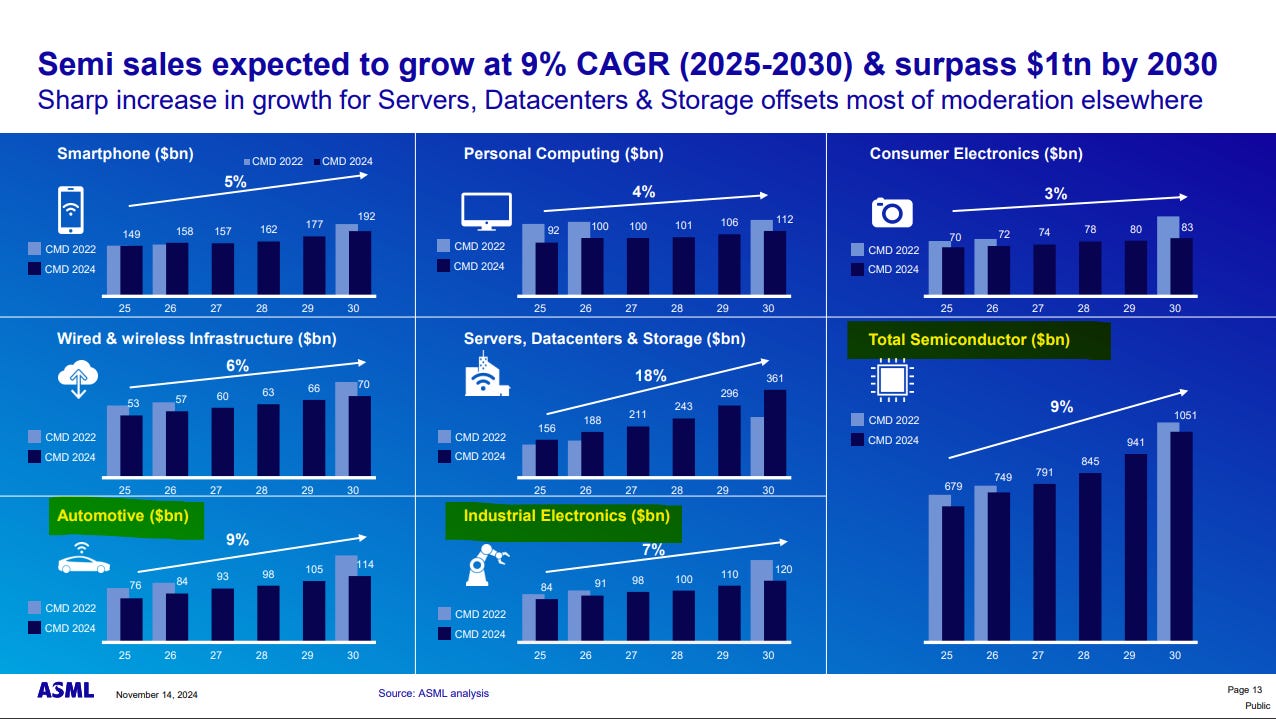

While TI is positioned in attractive end markets with a focus on Automotive and Industrial automation, ASML updated its guidance in 2024 and expects both segments to grow slower than they expected in 2022. Much of the growth in semiconductors is expected to come from servers, data centers and storage, while the other subsegments suffer more.

Margins (4/5)

TI has a low cost structure due to its inhouse manufacturing and investment into 300mm wafers. As their investment cycles comes to an end they’ll have 90% of capacity inhouse with most of wafers and testing inhouse as well. This enables margin expansion through vertical integration.

The strong operating leverage inherent in this business model is a double edged sword, as we’ve seen over the last few years: while TI benefits in a up-cycle, the down-cycle gets ugly with strong operating deleverage. This has been amplified by the counter-cyclical reinvestment into capacity, especially shown in FCF margins. We can’t forget the long-term margin potential of inhouse manufacturing however.

Balance Sheet (2/3)

The company has a strong balance sheet with 0.6x net debt/EBITDA. Debt has increased in recent years to fund the dividend and reinvestment through the down-cycle. It’s in a very healthy position and TI managed to get good interest rates on its debt.

Want the full investing experience?

In the next part I talk about the remaining 9 metrics, going over the competitive advantage, growth, reinvestment, predictability and valuation of Texas Instruments. Consider subscribing to Heavy Moat Investments and take your investment research to the next level.

🔥 I recently made my deep dive into Ashtead Group free—so you can see exactly what to expect: Business model deep dive - Fundamentals and Valuation deep dive

As a premium subscriber, you’ll get:

✔ Detailed Research on high-quality global compounders and European champions, with deep fundamental & valuation analysis.

✔ Actionable Investment Pitches – Ideas with high upside potential and limited downside.

✔ Earnings Breakdowns on key reports and market reactions.

✔ Real-Time Trade Alerts on all my portfolio moves, plus access to the premium chat.

✔ Exclusive Investing Tools, including my Inverse DCF template and more.