Free Sample - Ashtead: Consolidating the US equipment rental industry

Why own it if you can rent it?

This is a free sample of the in-depth research I provide to my paid subscribers. My goal is to give you valuable insights into high-quality businesses while making investing easier and more rewarding.

If you find this deep dive useful, I’d love to welcome you as a premium subscriber—so you can access all my research, exclusive insights, and tools to invest smarter. Let’s grow and learn together!

Ashtead was founded in 1947 as Ashtead Plant Hire Company Limited in England, a rental company for heavy equipment. In 1984, the company transformed to its current form, Ashtead Group PLC, to acquire a five-branch business with around 1 million pounds of revenue. This marks the beginning of its acquisition spree over the coming decades. In 1986, the company was listed on the London Stock Exchange. 1990 marks a transformational year after it acquired Sunbelt Rentals to expand its business into the USA. In the following decades, it had been fueled by organic growth and acquisitions in the US, including the sixth largest player at the time, NationsRent Inc., becoming the second largest equipment rental company in the US after United Rentals. 2014 marks the beginning of the expansion into Canada with the acquisition of GWG Rentals. Since then, the company has continued its strategy and recently presented its Sunbelt 4.0 strategy.

You can find the second part of the analysis here.

Business Model

Ashtead runs a heavy equipment rental business in the US, UK and Canada, with the US accounting for most of the business. In early 2024, the company operated 1,317 branches in the US, 763 of which were general tools and five specialty branches. These branches are used for storing and maintaining equipment. Customers rent equipment out and then it gets delivered to the location—a very basic business at first glance. The challenging part is the logistics around it and the various end markets. Ashtead invests in clustering its markets to increase its network effect, where multiple branches are operated closer to dense populations or strategic economic areas. This pushes all KPIs up and enables better cross-selling, as seen below and is thus highly attractive for Ashtead.

During the financial crisis, the company suffered (a 30% decline in revenue and no profits) and lowered investments in the business. While this preserved cash, in hindsight, they left much of the recovery behind, a mistake they don’t want to repeat. One reason for the suffering after the GFC was the large exposure to the construction industry. Ashtead typically is affected late into a cycle, so they have time to adjust investment levels accordingly. Ashtead has continually shifted its revenue mix towards non-construction revenue, which now accounts for around 60% of sales. Below are some examples of non-construction end markets Ashtead serves.

Specialty Rentals

A meaningful part of the past growth and diversification has been the focus on specialty rentals. These aren’t your traditional machines, but, for example, pumps to aid during flooding or sound equipment for a music festival stage. Specialty grew at a 25% CAGR in recent years, faster than the general tools business segment. Today, specialty accounts for roughly 1/3 of rental sales and is expected to experience further rental penetration (meaning the percentage of equipment that customers rent versus own) and growth over the coming years. Currently, specialty has only a 10% rental penetration versus around 50% for general tools. The trend is generally towards asset-light business models, and heavy equipment is a low-hanging fruit for most businesses to outsource and improve working capital.

🔒 This is where premium content would normally begin

If you enjoyed this free sample, consider subscribing to Heavy Moat Investments to get full access to all my deep dives, investment ideas, and exclusive insights.

As a premium subscriber, you’ll get:

✔ Detailed Research on high-quality global compounders, with deep fundamental & valuation analysis.

✔ Actionable Investment Pitches – Ideas with high upside potential and limited downside.

✔ Earnings Breakdowns on key reports and market reactions.

✔ Real-Time Trade Alerts on all my portfolio moves, plus access to the premium chat.

✔ Exclusive Investing Tools, including my Inverse DCF template and more.

Competitive advantage

The heavy equipment rental business is a very fragmented industry with thousands of small operators, often with just a single location. Companies with less than six branches comprise 50% of all locations. Industry players can unlock huge scale benefits by consolidating. There are several reasons why scale matters so much in this industry and why the large players will continue to become larger.

Firstly, having a larger presence and more locations can improve routing, which matters greatly if you transport heavy equipment. Proximity to the customer and the last mile of delivery is also worth a lot. Through clustering, Ashtead is looking to improve proximity and cement its leadership in the most attractive population and industry centers in its markets. Large enterprises often won’t deal with many small operators and will be served as national customers by one or two industry players.

Ashtead can split G&A costs and IT product development costs over a larger base and consolidated branches can benefit from better support systems and the brand name to fuel growth. Cross-selling between branches is another benefit.

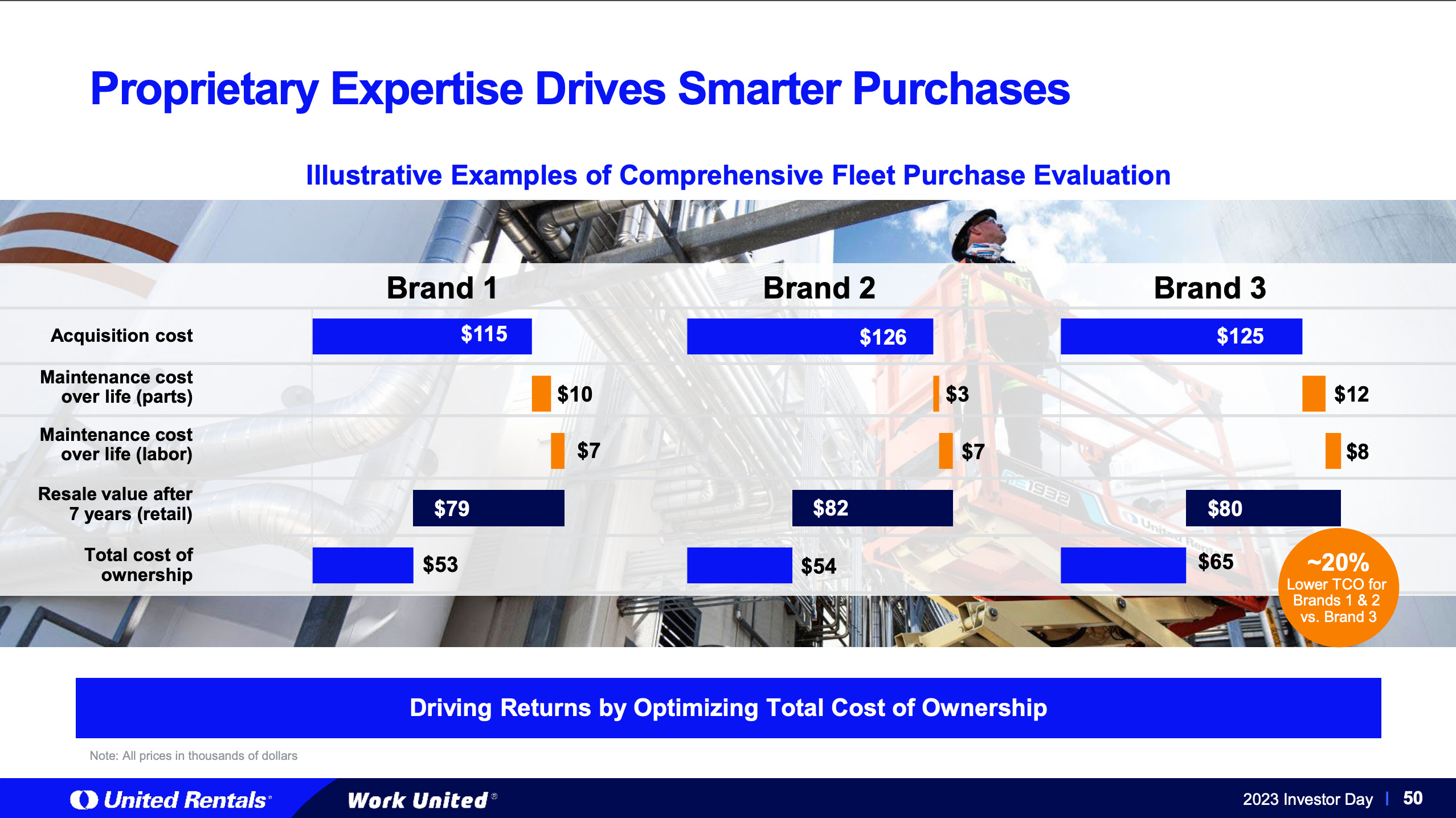

Lastly, let’s illustrate the equipment life cycle. I’m using this slide from United Rentals URI 0.00%↑, the industry's biggest player and another well-run company. URI and Ashtead spend billions each year buying new equipment from OEMs (original equipment manufacturers) to add to their fleet and replace old machines. This makes them some of the largest customers of companies like John Deere DE 0.00%↑ or Caterpillar CAT 0.00%↑ and gives them bargaining power. Maintenance cost is around 10-15% of the purchasing price over a machine's life cycle, and after seven years, the equipment is resold on average. Because of the favorable buying prices, Ashtead/URI can recoup around 2/3 of the purchase price and reinvest the proceeds into new equipment again. This is another evidence of the scale advantages inherent in this industry.

Tailwinds and reinvestment

The rental equipment industry is benefiting from several tailwinds. First, as previously mentioned, business models are becoming more capital-light and thus, the demand for rental over ownership increases throughout the economy. Second, the US has seen decades of underinvestment in infrastructure as well as structural shifts like reshoring and the CHIPS Act. This leads to a strong demand for construction and maintenance for the next decade and beyond. Ashtead should benefit from this dynamic.

Ashtead invests behind these trends and wants to cluster more of its markets. The reinvestment runway is large. We must remember that Ashtead is a very capital-intensive business. To maintain the $15 billion fleet, the company needed to deploy $2.1 in FY 2023, partially offset by $879 million of equipment sales. Furthermore, $1.6 billion was invested into growth capacity and another $0.8 billion into acquisitions. This organic investment depressed free cash flows, especially compared to rival URI. However, in 2020, Ashtead showed that they can gush cash if they reduce growth investments (something we don’t want to overdo as long-term investors!). URI is much more focused on large M&A deals than greenfield expansion. M&A deals are financing cash flow and do not affect free cash flows, so please don’t get fooled by URI’s much higher FCF: they simply invest through the financial instead of the operating part of the cash flow statement.

Management

Short-term compensation is based on EBITDA, specialty growth and operational improvements (rental revenue/average original equipment cost, customer satisfaction and ESG) alongside its Sunbelt 4.0 targets.

Long-term compensation is tied to total shareholder return (40%), EPS (25%), ROI (25%) and leverage (10%, target range of 1.5-2 times EBITDA). Overall, 88% of CEOs and 83% of NEOs pay is at risk, based on these criteria. I love most of this compensation structure as it covers growth, operational efficiency and other KPIs, capital efficiency (ROI) and leverage, something you don’t often see in compensation structures. Management has a good track record of growing the business profitably while not overleveraging.

The big downside, however, is the lack of insider ownership, with just 0.2% of shares outstanding in the hands of insiders. Rival URI has a similar weak 0.4% insider ownership and a similarly good compensation structure: short-term based on EBITDA and economic profit growth (ROIC-WACC spread) and long-term revenue growth + ROIC.

Conclusion

Ashtead is a well-run industrial company in a fragmented industry with clear scale advantages. Eventually, two or three players will command half of the market (currently 30% between URI and Ashtead). After owning it for a bit, I realized the business is too capital-intensive for me. Both companies are on my watchlist in case they get really cheap again. Secular tailwinds will enable a long runway of profitable growth and consolidation. While the US is the majority of the business, the UK and Canada offer additional growth opportunities at a smaller scale, thus less attractive.