ASML Valuation update

Attractive after a 30% drawdown trading at 22x NTM EV/EBIDTA?

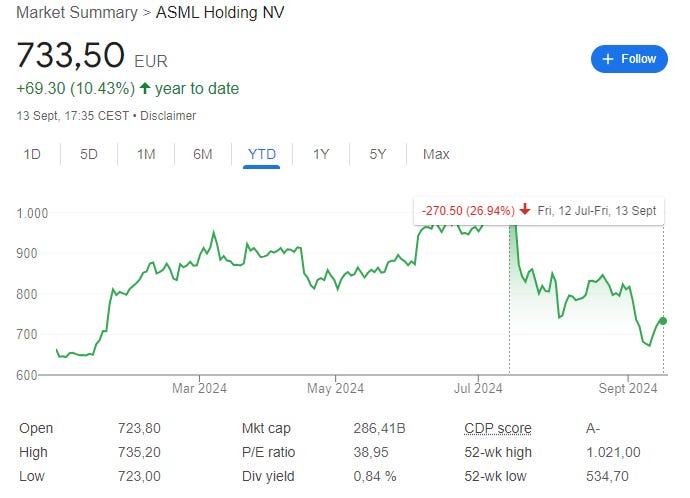

ASML has given up most of its year-to-date gains and is currently in a 27% drawdown. The company ranks highly on my quality score with 46/63 points and has one of the deepest moats out there. Let’s update the valuation on ASML with a multiple-based, inverse DCF and IRR model approach.

The good thing about ASML is that it’s a predictable business over a cycle. Although in a cyclical industry, there is a long-term secular trend for increased semiconductor demand and complexity. Most secular trends rely on chips to power them. ASML carved out a monopoly in the high-end manufacturing of all chips, and there is no sign of competition penetrating the market for EUV lithography. This allows ASML to plan long-term with its key EUV customers: TSMC, Samsung, Intel, Micron and SK Hynix. One risk I’d address here is Intel’s struggles. As a key customer, I would find it bad to see Intel cancel manufacturing projects. However, the demand is there and somebody will build a fab and install lithography machines. This predictability makes me confident that ASML’s 2022 Investor Day projections are sound and can be used to project the business and its range of possible outcomes. One could argue that after the investor day, the AI hype broke over the world after ChatGPT was announced and elevated ASML’s growth profile, but I’d prefer not to extrapolate too much here.

Ready for More?

By becoming a paying subscriber, you can read the rest of this article and all of my writing on businesses, valuations and investing. Don't miss out on the opportunity!

Subscribe now and get 15% off your first year using the code below: