Capital-Heavy versus Capital-Light

Which business model should we prefer?

Today, I want to discuss a central concept in investing: capital-light versus capital-heavy business models. How can we differentiate between the different models? Which should we prefer? What are the implications of each model? Let’s get right to it. We can also use asset-light/asset-heavy or variations as a term.

Defining the terms

Assessing a business model is a critical part of qualitative analysis. Different businesses require different amounts of capital to run. This is what capital light or heavy refers to. Let’s take the example of NextEra Energy, one of the US's largest renewable energy utility companies. We can see that the business generated $7.5 billion of net income on $27 billion of revenue. However, free cash flow is negative, at $14.8 billion. That’s because the business has an incredibly high capital intensity, making it very capital-heavy. NextEra is an extreme example of a capital-heavy business with CapEx as a percentage of revenue above 100%. The income statement doesn’t include capital expenditures; we only see the accounting profits. As investors, we want to know the cash profits, though. After all, that’s what the company can reinvest or return to owners. Capital-heavy businesses usually have a wider gap between net income and free cash flow. This concept is called the cash conversion. We want as much net income to convert to FCF as possible, ideally over 100%.

One caveat: After we notice high CapEx as a percentage of revenue, we should guess how much of it is maintenance versus growth CapEx. Large periodic investments in growth CapEx should be viewed differently than maintenance CapEx.

On the other hand, we can look at financial data services company MSCI Inc.: the company generates $1.17 billion of net income on $2.6 billion of revenue and converts over 100% of net income to FCF. This is a very capital-light business, requiring next to no CapEx to run the business (under 1% of revenue).

Capital-heavy Pros and Cons

From the first impression, capital-heavy seems like the much worse option, but let’s start with the positive. Capital-heavy businesses tend to benefit the large players, allowing them to defend their market position more easily. New competitors can’t come in without having to invest a lot of money, which is hard to get, especially in a higher interest rate environment. Often, buying up a lot of land and building a ton of factories, retail stores, or data centers is not a viable option, so new competitors rarely emerge.

Capital-heavy businesses require lots of capital to run, especially for maintenance CapEx, which means replacing or repairing infrastructure, machinery, servers or whatever they invested in. This reduces free cash flow and thus the amount of capital left to reinvest into other parts of the business or return to owners. These businesses can also look deceivingly cheap if one only looks at EV/EBITDA or P/E ratios: due to the large depreciation expenses, EBITDA is usually high, and the P/E ratio does neither account for the CapEx nor the high debt levels that capital-heavy businesses often carry. We should always have the cash conversion in mind because we don’t want accounting profits but real cash flows.

Capital-light Pros and Cons

Capital-light businesses benefit from low-maintenance CapEx needs. This means they usually have high cash conversion rates and lots of free cash flow to reinvest in the business or return to owners.

New competitors can enter a market much more easily without a sizeable upfront investment and capital needs. Capital-light companies need a clear competitive advantage in their brand, technology or network effect to stand out, keep and grow their market share.

Cash conversion cycle

A factor I want to talk about separately is the cash conversion cycle. It’s a concept I’ll cover in more detail soon, but to quickly sum it up it’s a metric that measures how fast a company can convert products into sales and cash flow. It sums up days of inventory and days of sales outstanding and subtracts days of accounts payable. A shorter cycle means that we tie our capital up for shorter times. A negative CCC even means that our suppliers pay for our investments (we pay them after we already converted the product into cash flow). This is a powerful dynamic and capital-heavy companies often have longer cycles: they often require significant levels of inventory and have long sale cycles (think about a large industrial machine, which often takes months to complete, ship and then book the revenue). Capital-light businesses, on the other hand, often don’t have these problems. Both types can leverage long accounts payable cycles to improve their cash conversion cycles, this often happens if a company has a lot of bargaining power over its suppliers.

Which should we prefer?

According to EY, we should undoubtedly prefer asset-light businesses. In a study of the S&P 500, they found that asset-light companies outperformed their asset-heavy peers over the last five years by four percentage points based on total shareholder return. However, as with everything in investing, it is more nuanced. The ideal business requires next to no capital to grow while growing its competitive advantage and reinvesting its excess cash at high ROIIC or returning it to shareholders. However, very few are close to ideal businesses and they are often very expensive (MSCI is an example of an excellent business).

Asset-heavy companies can have strong and growing moats, ideally they are only partially asset-heavy during large investment cycles and then reap the rewards as they grow into their assets. Amazon's performance after its jaw-dropping $250 billion in Capex investments since the Covid pandemic hit is a good example. Where it gets tricky is companies with large maintenance CapEx requirements which eat up all the cash flow that could be returned to owners. Those businesses should be avoided in most cases. What I want to do with this article is to raise investor’s awarness and to study the capital intensity of each company they look at. We can then conclude if we want to own a company with that level of maintenance requirements. At the end of the day, great businesses are found on both sides of the spectrum, and we have to decide for ourselves.

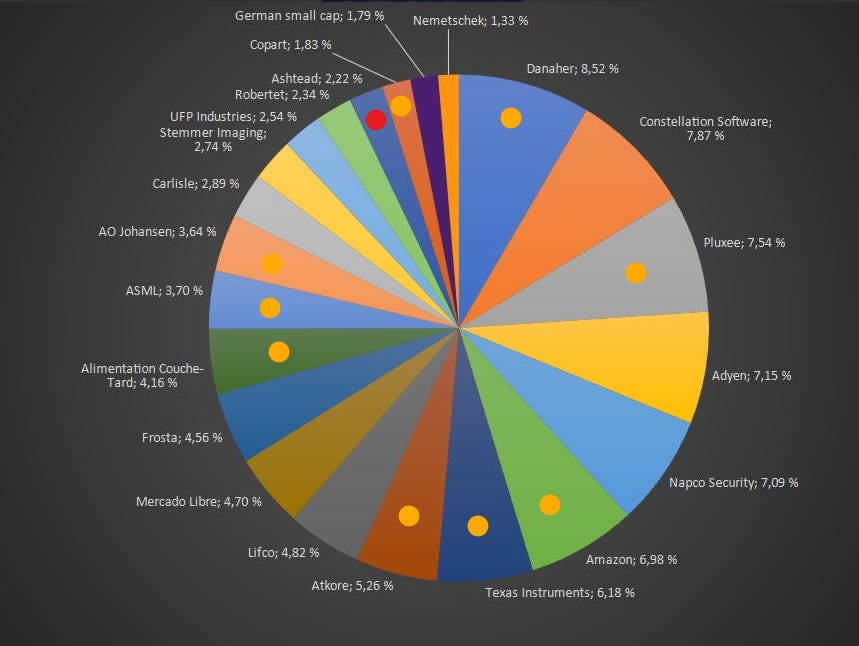

A look into my portfolio

Let’s take a look at my most recent portfolio update. I added colored dots to the positions where the capex exceeds 5% of revenues. We can see that a large portion of my portfolio has moderate capital intensity. Fortunately, all of them invest a large amount of CapEx into growth investments. Ashtead stands out as by far the most capital-intensive business. Out of $4 billion in operating cash flow, the company requires $1.9 billion in maintenance CapEx. The company rents out large industrial equipment, which is inherently capital-heavy. Recently, I’ve been pondering if I want such an asset-heavy business in my portfolio, and I’ll review these questions in an upcoming analysis of Ashtead.

I hope that you found this article useful. Please consider supporting my work by sharing or becoming a premium subscriber. The button below offers 15% off the first year. Read more about the benefits here.

Depends on the goal actually.

Asset light businesses are superior in terms of growth thus they can increase your portfolio value rapidly, though they are more open to disruption.

If you are looking for just above market returns consistently, than the dominant asset intensive business will likely do the job.

Super interesting! Great analysis.