Verra Mobility (VRRM): Fundamentals and Valuation

Verra Mobility has been public for five and a half years and has outperformed the market with a 17% CAGR. The shares struggled following the pandemic as people feared the impact of closed airports on the US rental car fleets (a large part of the customer base) and lower traffic. Since 2023, VRRM started to outperform and has been in a strong rally. Let’s look at Verra's fundamentals and valuation. You can find the first part of this deep dive here.

Growth

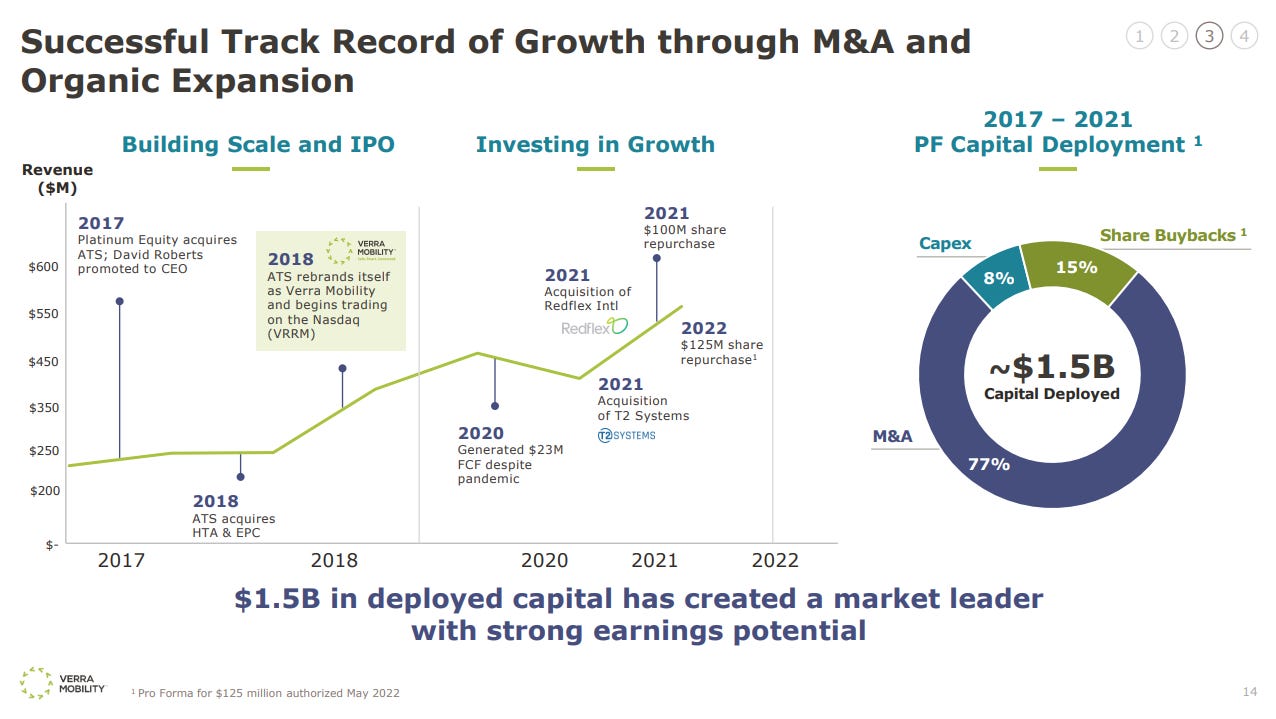

Verra has been a strong growth story over the last five years since going public. Revenues grew at 16% CAGR, EBITDA at 11% and EBIT at 21%.

While Verra operates in structurally growing niches with expected long-term organic growth in the high single digits, M&A has played a large part in their strong growth. The company has spent over $1.1 billion on M&A since going public and has diversified its revenue base. Covid also distorted growth because, obviously, Verra’s business was severely depressed in 2020. A lot of business comes from fleets, highly dependent on air traffic, which was shut down for most of 2020. There are many targets left for Verra to use the previously discussed M&A framework to enhance its value creation for shareholders.

Premium Offering

Consider subscribing to Heavy Moat Investments to get the full experience and improve your investment journey. As a premium subscriber, you get:

Investment research into global high-quality/compounder companies, primarily in the Small/Mid-cap range ($100 million to 20 billion), split into business model and fundamental & valuation analysis.

Earnings analysis on interested earnings reports (often after a strong reaction in the stock price or unexpected fundamental developments).

Notified about all my transactions on the same or next day and a premium chat.

My Inverse DCF template and other resources.